New swing systems and portfolios

The MeanSwing strategy is now officially released. There are two systems: MeanSwing ES NQ applies the MeanSwing strategy to the emini futures of the S&P 500 and Nasdaq 100, and MeanSwing Indices applies the MeanSwing strategy to all five US emini stock index futures (S&P 500, Nasdaq 100, Dow Industrials, Russell 2000 and S&P MidCap 400). There are four portfolios that include these new systems as well – click here and scroll down to the “Index Trader” portfolios.

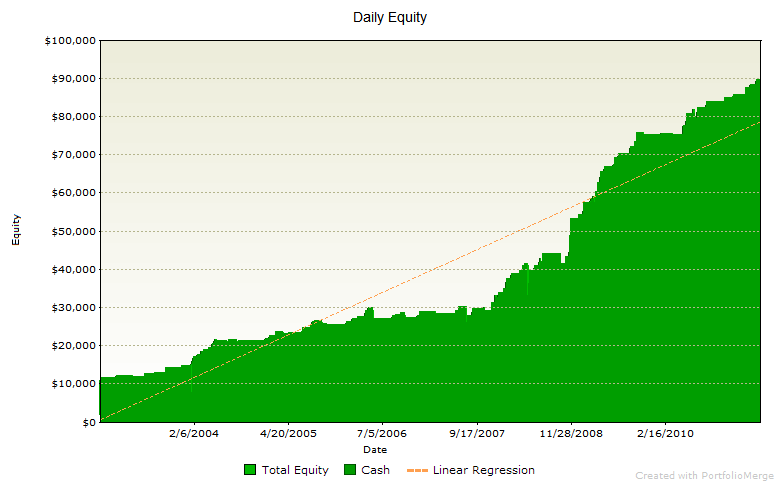

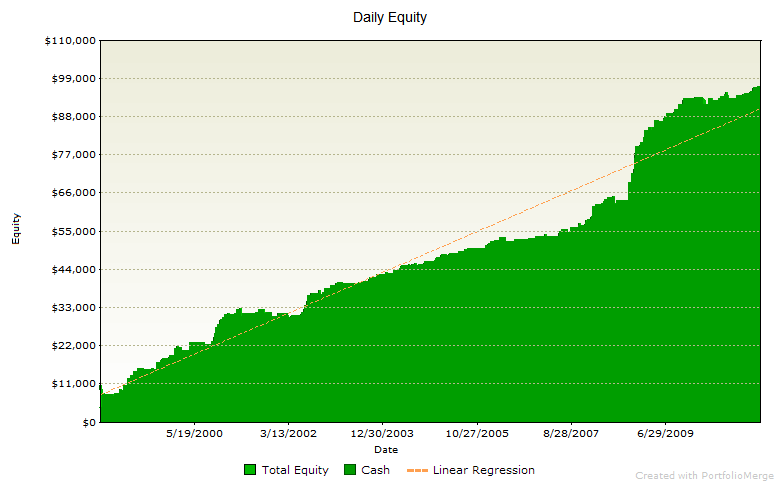

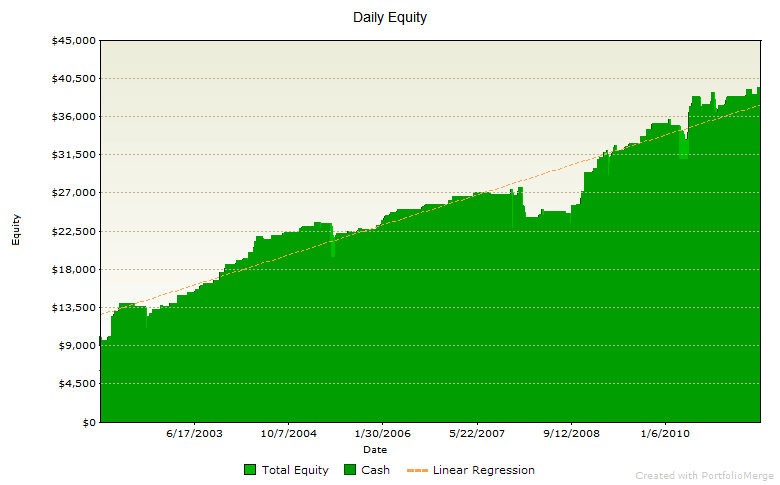

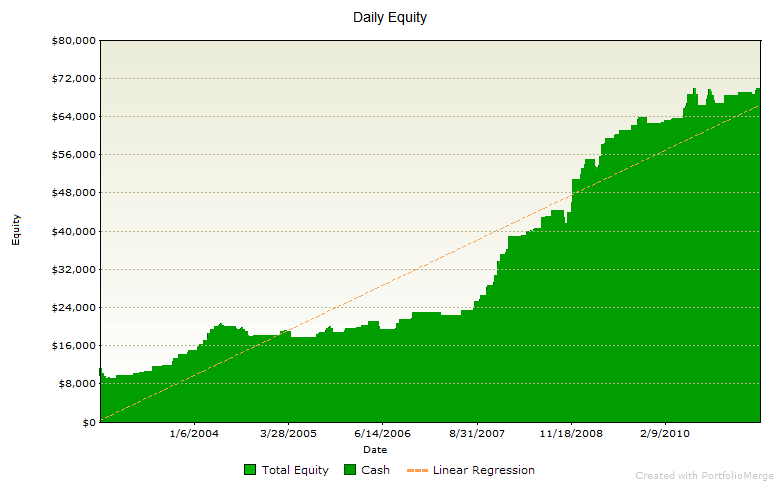

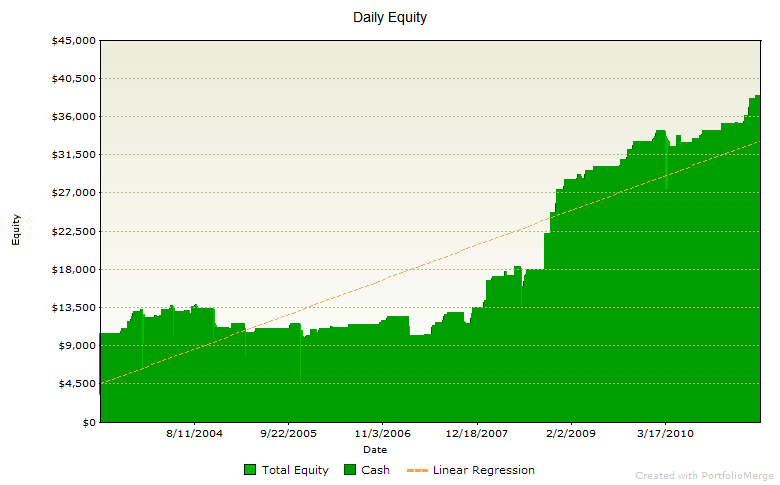

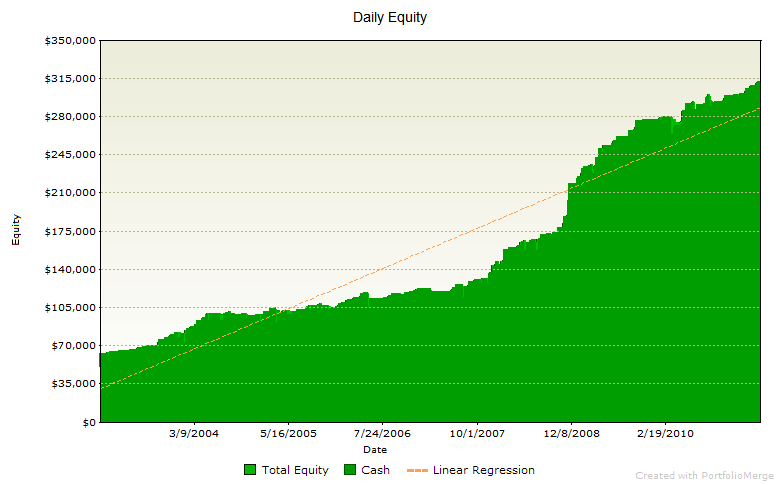

This swing strategy is the result of my looking to create a system that performs well when the intraday trend-following strategies are performing poorly. The result is a mean-reversion (counter trend) swing system that has performed well not only when the intraday trend-following strategies are performing poorly (so far in 2011 MeanSwing has a gain in every index) but also for the entire history of each index future. Here are the equity curves for the entire history of each emini index future (see Disclaimers link in top menu, past performance is not necessarily indicative of future results). The final equity curve is all indices combined.

And how does MeanSwing do when combined with the intraday strategies? Pretty well in my opinion. There is low correlation which provides the desired diversification. In fact the drawdown for the portfolios with MeanSwing Indices (Index Trader III and IV) have a lower historical max drawdown than the system alone since they are combined with intraday strategies. Please take a look at the Portfolios page for more information.